)

)

)

Edge20 Mar 2026

Tetra Pak: The Shape of Innovation

The story of Tetra Pak, the Rausing family, and how a paper tetrahedron gave rise to a company that now delivers almost 180 billion packages a year.

In 1971, a grocery store owner outside Oslo complained to a sales representative about his empty bottle problem. Months later, the solution to that complaint became TOMRA. More than fifty years on, TOMRA has grown into the world's leading provider of resource optimization technology: the infrastructure behind deposit return systems on six continents, the sorting machines inside the largest recycling facilities, and the grading systems that process the majority of the world's french fries. What started as a machine for one local store now sits at the center of the circular economy.

For decades, waste was largely treated as the end of a product's life cycle. Increasingly, however, governments, industries, and consumers are approaching materials differently, as resources to recover, sort, and return into circulation.

TOMRA has spent more than fifty years building technology at the center of that transition. What began with reverse vending machines (RVM) for returned beverage containers has expanded into a global business built around different aspects of the circular economy. Today, the company's systems are used to identify, sort, grade, and recover everything from plastic bottles and aluminum cans to industrial waste streams, potatoes, and blueberries.

Across the TOMRA group, the same underlying logic has driven every expansion: solve a practical problem, build technology around it, and adapt it market by market.

Before writing this article, we had the opportunity to sit down with TOMRA CEO Tove Andersen to discuss the company's history, culture, and the road ahead. Throughout our conversation, TOMRA's operational focus turned us back to core themes of decentralization, adaptability, and maintaining the entrepreneurial mindset that has shaped TOMRA since its founding in 1972. Reflecting on the company's culture, Andersen said: “The person closest to the problem is typically best at solving it.”

In many ways, that philosophy and how it scales in an organization of over 5,000 employees explains both how TOMRA operates today across its global divisions and the mindset that has shaped its history. Coincidentally, it also captures how the company began more than fifty years ago.

The history of TOMRA begins with two brothers, Tore and Petter Planke, from Asker, a small town just outside Oslo. In 1971, Petter was working as a sales representative for labeling and pricing equipment, visiting supermarkets across the Oslo area. One of his regular customers was grocery store owner Aage Fremstad. A conversation Fremstad initiated that year would change the trajectory of both brothers' lives and, eventually, global recycling infrastructure.

“We are drowning in deposit bottles, all kinds of bottles, and there's coming more and more varieties of them. So you need to help us to sort that out."

Like every retailer in Norway, Fremstad was legally required to accept returned beverage containers. The obligation dated back to 1902, when Norway established one of the world's first deposit return systems for reusable glass bottles. The arrangement, created voluntarily by the beverage and grocery industries, was built on a simple idea: when customers bought a glass bottle, they paid a deposit, which was then returned to them when the bottle was returned to a retailer.

For decades, the system worked reasonably well. Glass bottles came in relatively few formats and were manageable for retailers to handle manually. But by the late 1960s, the complexity was growing. Bottle formats multiplied: different sizes, shapes, producers, and deposit values. What had once been a manageable back-room task became a logistical burden, with employees spending hours counting and sorting containers while storage areas filled with unsorted glass. Breweries, bottlers, and retailers had all tried to find a solution, without success.

Before returning to the Planke brothers, it is worth noting that Norway's deposit system at the time applied only to reusable glass bottles that were collected, cleaned, and refilled rather than crushed and recycled into new ones. The concept of a single-use container – the plastic bottle or aluminum can that would come to define modern deposit systems – would come later. When they arrived, they would dramatically increase both the scale of the problem and the opportunity for the machine the brothers were about to build.

Petter told his brother, who was an engineer by trade, about Fremstad's problem, and Tore began developing a prototype in his spare time. The design the brothers eventually settled on featured a single opening through which any bottle could be inserted, an automated recognition system capable of identifying different container types, and a printer that issued a receipt for the deposit value owed. For its time, it was highly advanced engineering, combining sensor technology, mechanical handling, and early computing.

The first reverse vending machine was loaded into the back of Petter's Renault 16 and delivered to Fremstad's store on January 2, 1972. The response was immediate. Fremstad called it his best investment, and customers loved the convenience of feeding bottles into a machine and receiving a receipt instead of handing containers to store employees over the counter.

Sensing they were onto something, the brothers immediately began producing more machines, and within just the first couple of months, they had sold 15. Since the same problem existed beyond Asker, the opportunity did as well. On April 1, 1972, Tore and Petter Planke officially founded TOMRA.

The name TOMRA comes from the acronym TOMflaske Registrerings Automat, Norwegian for “empty bottle registration machine,” pragmatically explaining the function of the RVM. From the beginning, the Planke brothers believed recovering and reusing material served a broader purpose beyond the convenience of the machine itself.

Still, in the early years, TOMRA's focus was narrow: retailers needed a better way to manage returns, and the brothers had built a machine that solved the problem. Over time, the scale of what deposit systems could achieve would become central to the company's identity.

By the end of its first year, 29 machines were operating across Norway, driven by retailers facing the same problems that Fremstad had described to Petter. Tore's technical expertise and Petter's commercial instincts proved a perfect combination as they scaled the family enterprise beyond Asker.

The first major signal that TOMRA's idea could travel came from just across the border, where Sweden had long operated a similar system of reusable glass bottles with deposits. Systembolaget, the Swedish state alcohol monopoly, was legally required to accept returned containers just as Norwegian retailers were. In 1974, it ordered 100 TOMRA machines, specially adapted to fit the conveyor equipment already installed in its stores.

The order validated both the technology and the opportunity ahead. If the same inefficiencies existed beyond Asker and beyond Norway, why not expand into every market with a deposit return system? In the years that followed, TOMRA established subsidiaries in Sweden, Finland, Denmark, the Netherlands, and Germany – markets where deposit systems were already in place and manual handling was ready for an upgrade.

The next leap came from inside the machine itself. Early reverse vending machines had to be manually programmed to recognize specific bottle types, an approach that became increasingly impractical as beverage formats multiplied. In 1977, TOMRA launched the TOMRA SP, the world's first self-programmable reverse vending machine. Using laser, fiber optic, and microprocessor technology, the SP could recognize and adapt to new container types without manual reconfiguration.

The Planke brothers and TOMRA had been pioneers from the start, but the SP established a clear technological lead and laid the foundation for the company's next phase of growth.

In 1984, TOMRA continued its momentum across the border as Sweden expanded its deposit system to include aluminum cans, making it the first country in Europe to legislate a deposit return system for single-use containers.

For TOMRA, it was a major opportunity. Roughly 2,000 retailers suddenly needed machines capable of accepting cans before the law came into effect, only months away. Petter later recalled: “We were even sleeping on couches in the job, we were working 24 hours a day. It was crazy – but we did it.”

With growing momentum in Europe and fresh capital from its 1985 listing on the Oslo Stock Exchange, TOMRA entered the U.S. market. The timing appeared attractive: aluminum can consumption was rising rapidly, and several states had recently passed bottle deposit legislation. For a company looking to expand into the world's largest beverage market, the opportunity was difficult to ignore.

However, the market dynamics turned out very differently from what TOMRA had expected. In 1985, the Soviet Union flooded global commodity markets with aluminum, cutting prices by more than half within months. In much of Europe, deposit systems were driven by legislation, which meant collection targets and machine demand held regardless of commodity prices. In large parts of the U.S., however, recycling economics were the primary incentive behind collection, and when aluminum prices collapsed, so did much of that incentive. A year later, TOMRA exited the U.S. with substantial losses and some very valuable lessons.

In hindsight, the episode was an important turning point in the company's history. The failed U.S. expansion clarified where TOMRA's Collection business was strongest: markets anchored by deposit legislation and return systems, where collection volumes were driven by regulation rather than commodity prices or recycling economics. That distinction continues to shape the company's strategy to this day.

Following the listing and expansion efforts, the Planke brothers, who had built TOMRA from a single machine into a publicly listed international business in just fourteen years, sold their stakes and stepped away from the company. Though neither retained an operational role, both remained closely connected to TOMRA over the decades that followed. More than fifty years since its founding, with headquarters still in Asker, the culture and mindset established by Tore and Petter continue to shape the company.

In the depth of my heart, I just love what I see in TOMRA today, and the way TOMRA is flourishing in this field.— Tore Planke, 2017

Refocused on Europe, TOMRA quickly returned to profitability. As deposit legislation expanded and the installed base grew, the company regained momentum through the late 1980s.

At the same time, the machines themselves continued to evolve. Building on the advancements of the SP model, TOMRA continuously expanded the machine's capabilities as beverage packaging became increasingly fragmented. Aluminum cans, plastic bottles, multi-packs, crates, and new bottle formats all entered deposit systems, each bringing new operational and technical demands that TOMRA adapted to.

Over the years, the technology advanced significantly. Laser-based recognition, barcode scanning, weight detection, integrated crushers, metal detectors, and eventually remote connectivity were gradually added to the machines. By the early 1990s, TOMRA was the only manufacturer in the world offering reverse vending machines capable of accepting all major beverage container types.

Less than a decade after its previous attempt to take on the U.S. market, TOMRA returned with a clear strategy. Rather than operating broadly in voluntary recycling markets, TOMRA concentrated entirely on the ten US states that had passed return obligations in their bottle deposit legislation.

As part of its reentry, TOMRA acquired several local material handling and collection operators across the northeastern United States. One of them, NEROC, marked an important step beyond the company's traditional business of selling and servicing reverse vending machines. Through these acquisitions, TOMRA expanded further into processing, material trading, recycling, and container production, moving deeper into the value chain.

The more focused U.S. strategy proved successful. By the end of the 1990s, the United States had become TOMRA's single largest market, accounting for more than half of the company's revenue. By then, the company had grown into a global business operating in 34 countries with more than 1,700 employees.

If Sweden's 1984 can legislation was the first demonstration of what deposit mandates could mean for TOMRA's order book, Germany in 2006 proved it at a scale far beyond anything the company had experienced before.

Germany had introduced a national deposit system for non-refillable containers in 2003, but the initial rollout struggled because the system was poorly designed and failed to create sufficient incentives for consumers to return containers. The framework was revised and substantially improved in 2006. TOMRA, still the clear technology leader in reverse vending, was uniquely positioned to supply that opening.

The factories ran at full capacity, the logistics operation was enormous, and the rollout became one of the defining moments in TOMRA's history. In that first year alone, the company delivered approximately 8,800 reverse vending machines to Germany – roughly three times its normal annual global sales volume at the time.

The German rollout demonstrated how quickly regulation could reshape TOMRA's business and led to a market position that the company still holds today. With more than 30,000 installed reverse vending machines, container return rates around 98%, and decades of recurring service revenue flowing from that installed base, Germany remains TOMRA Collection's largest market.

Around the turn of the millennium, the reverse vending machine continued to evolve alongside the markets it served and the constant introduction of different beverage packaging. When lightweight plastic bottles became the norm and toppling inside the RVM became a problem for consumers, TOMRA's answer was to create a machine that accepted bottles lying down, a design feature that would remain part of its machines for decades.

For more than thirty years, the company's strategy had been straightforward and successful. TOMRA had built a global business around the reverse vending machine, expanding market by market as deposit legislation spread. By the mid-2000s, however, the company began looking beyond its core family of machines. The expertise within the organization and the potential applications of its sensor-based recognition technology across adjacent areas of the value chain inspired a series of acquisitions in the years that followed.

The first and most consequential move came in 2004 with the acquisition of TiTech Visionsort, a Norwegian company specializing in optical sorting technology for mixed waste streams. TiTech's systems could separate plastic, paper, metal, and glass at industrial recycling facilities using advanced sensor-based recognition.

It was followed by the acquisitions of Orwak Group in 2005, Commodas in 2006, and Ultrasort in 2008, each adding capabilities across waste sorting, metals, and mining. Together, these acquisitions laid the foundation for what would eventually become TOMRA Recycling.

A few years later, TOMRA took the next major step toward becoming the group it is today. Collection had benefited enormously from the global expansion of deposit legislation, but growth still depended heavily on regulatory timelines. Germany had demonstrated the scale of a successful legislative rollout, yet many other markets were moving far more slowly.

The European Union had introduced directives encouraging higher recycling rates, but without binding mandates, many governments delayed implementation. New deposit markets continued to emerge around the world, though often gradually and years apart.

TOMRA had built a large installed base that generated recurring service revenue on top of machine sales and upgrades, but growth through new equipment sales remained uneven. The company's long-term belief in Collection was unchanged, but applying its core competencies to other, less legislation-dependent growth areas made strategic sense.

The move into Recycling was the first expression of that thinking, and the next step expanded it further. In 2011, TOMRA acquired Odenberg, an Irish company focused on optical food sorting and processing, with leading positions in categories such as potatoes, vegetables, dried fruit, and nuts. With more than 2,000 optical sorting systems installed worldwide, Odenberg became the first in a series of acquisitions that would, down the line, lead to TOMRA Food.

As with Recycling, the rationale was rooted in TOMRA's deep experience in sensor-based recognition and sorting technology. After Odenberg, TOMRA acquired a complementary food sorting technology manufacturer BEST Sorting in 2012, followed by Compac in 2016 and BBC Technologies in 2018. Each added new expertise and strengthened the group's position in food sorting and grading.

Food gave TOMRA another growth stream, one driven by commercial needs. The timing also made sense: global population growth, higher food prices, stricter food-safety requirements, and growing demand for supply-chain traceability all pointed toward a greater need for automated sorting and quality-inspection technology.

At the time, Food joined Recycling within the newly created TOMRA Sorting Solutions, which replaced the earlier Industrial Processing Technology structure. From 2020 onward, the businesses were separated into the three core segments the group has maintained since: TOMRA Collection, TOMRA Recycling, and TOMRA Food.

TOMRA has expanded far beyond its first machines and the reverse vending segment itself. Still, Collection accounts for the majority of group revenue, and the reverse vending machine remains what most people associate with the company. Before turning to the broader business model, it is worth understanding what the machine actually does and what its current forms looks like.

The strength of a deposit system is that it creates what is often referred to as a “clean loop.” Unlike curbside collection, where containers are thrown into a mixed bin, contaminating the plastic before it even enters the recycling chain, a deposit system keeps the loop closed. The nudge of a return deposit means the container is handled separately, remains uncontaminated, and follows a controlled process from the moment it is returned all the way through to becoming a new bottle. The output is food-grade recyclate, pure enough to go straight back into food and beverage packaging.

If you live in Northern Europe, or in any of the growing number of countries with deposit return systems, you have almost certainly used one. For most people, it is simply a machine near the supermarket entrance: you feed in bottles and cans and receive a receipt in return. What happens inside during those few seconds is less visible.

The machine identifies the container through a combination of shape recognition, weight detection, barcode scanning, and optical analysis. The deposit value is verified and added to a running total. The container is then sorted, crushed if it is aluminum, compacted if it is plastic, separated if it is glass, and stored until collection. The entire process takes seconds and is repeated tens of billions of times each year across more than 90,000 machines in over 60 markets.

TOMRA's machines have continued to evolve alongside the complexity of modern beverage packaging. Over time, the company expanded its capabilities through advances in recognition software, barcode scanning, compaction, and remote connectivity, while broadening the range of containers a single machine could handle.

One of the most important technological leaps in recent decades came in 2013 with the launch of TOMRA Flow Technology, the world's first 360-degree instant recognition system for reverse vending machines. Containers no longer needed to rotate inside the machine before being identified, allowing them to move through in a continuous flow. The technology remains a core part of TOMRA's machines today.

In 2019, multi-feed return followed: consumers could now pour full bags of containers into the machine at once rather than feeding them one by one. For large retailers, the reverse vending machine increasingly shifted from operational infrastructure to a competitive differentiator as a reason for consumers with a week's worth of empties to choose one store over another.

We always adapt to local requirements.— Tove Andersen

Ever since its first deliveries in the 1970s, TOMRA's machines have been shaped through close collaboration with customers. The first machine solved a specific problem for a single retailer. The machines that followed were adapted to the needs of different markets. Over time, that responsiveness became as defining to TOMRA as the technology itself.

A TOMRA reverse vending machine in Hamburg, New York, or Melbourne will not look or operate the same. Each reflects the market it serves: the container formats in scope, the retail environment, consumer behavior, and even the climate. TOMRA CEO Tove Andersen, gave us an example of how those factors contributed to the company's adaptation in the Polish market:

“We always adapt to local requirements. In Poland, many of the retailers have very small stores and don't want a reverse vending machine inside the store because they have no space. They wanted an outdoor solution. Typically, you could build a shed and put the machine in there. But we have developed a new outdoor solution that doesn't need a shed. It can stand outside and handle very cold and very warm weather.

We had an outdoor solution from the U.S., but the weather conditions in Poland are colder than those on the East Coast, so we adapted the machine to local conditions. That's what I mean by leveraging global expertise but adapting to local need, which I think we have been very good at.”

That adaptability also extended to how TOMRA structured its offering across markets. Legislation differed, customer needs differed, and consumer behavior differed, so the commercial model evolved accordingly. In some markets, TOMRA sells machines directly to retailers. In others, it owns and operates the infrastructure itself, and in certain regions, it also manages logistics and material processing. Andersen discussed how that experience has shaped TOMRA's position within the industry:

“We have so much experience with what works well and what doesn't. When you initiate a new deposit market, you know what the key things to reflect on are and what will make it a success. We've collected all of this knowledge from all of these markets and based on that, developed key principles for launching a new deposit market, which we share with all interested stakeholders, from governments to the beverage industry, legislators, and others.”

The culture behind that adaptability was established early and still shapes the company more than fifty years later. The Planke brothers operated by a simple philosophy: “better today than yesterday, but not as good as tomorrow.” R&D, like the business itself, is spread across the group's global division hubs.

But Collection's R&D and TOMRA's headquarters remain in Asker, a short distance from where Tore built the first prototype. The company has grown far beyond the local retailers it originally served, but much of the culture established in those early years remains intact.

“We're influenced by Norwegian culture: very down-to-earth and non-hierarchical. There's no separate parking spot for me. Anyone can call me. All managers will pitch in when needed. That's the backbone. At the same time, TOMRA is much more international. From day one, Tore and Petter Planke were thinking internationally. So we're a good mix: a bit down-to-earth, non-hierarchical Norwegians, but with a truly global vision.”

– Tove Andersen

TOMRA's business model has been shaped by long-term trends aligned with its core purpose. Regulation has been central from the beginning, but broader shifts toward automation, industrial efficiency, and resource optimization have also become important drivers across its segments. Together, they help explain both TOMRA's history and the opportunities ahead. Across its divisions, the company today has nearly 120,000 installations in more than 100 countries.

The company operates across the three aforementioned core divisions – Collection, Recycling, and Food – each serving different customers, industries, and regulatory environments. But beneath those differences sits the same underlying capability: sensor-based object identification and sorting. The technology stack evolves across applications, but the core competency remains shared across all three segments. Tove Andersen expanded on how TOMRA views the group and its operating structure:

“First, what is the common denominator across TOMRA? Everything is about resource optimization. Everything is about sensor-based solutions for doing that. And every segment we operate in is global, where we can take a leading role.

Our operating model, I call it that we are a strategic family builder. That's what we call ourselves. We are a family. We have an overarching strategy for TOMRA. We have the same vision and mission for everything, but also overall targets and strategic focus areas, and more. We also have empowered children in this organization: the three divisions, with end-to-end responsibility.”

What the divisions ultimately share is a business model built around longevity: machines with lifetimes measured in decades, service relationships that deepen over time, and in some markets, infrastructure that TOMRA owns and earns recurring fees from based on usage. Let's go through those, one division at a time.

)

Collection is the consumer-facing end of TOMRA's business, built around the infrastructure that enables deposit return systems across markets. The division operates across more than 60 markets and accounts for roughly 55% of group revenue. In 2025, more than 53 billion beverage containers were collected through TOMRA's systems. Yet that still represented less than 3% of global beverage container consumption, highlighting how much runway remains as deposit systems continue to expand.

Despite increasing competition in newer markets, TOMRA has maintained a market share above 70% as recently as 2024, reflecting the position it built over decades through early market entry, scale, and technological leadership. The Collection business itself operates through several different commercial models depending on the structure of each market.

The primary catalyst for growth in Collection is legislation. That has been true since TOMRA's founding and remains true today. Deposit return systems are regulatory constructs by design: a government or designated authority places a deposit on beverage containers and requires those containers to be collected and returned.

That obligation – whether placed on retailers, beverage producers, or a central system operator – creates the infrastructure around which TOMRA builds its business. As seen throughout its history, without regulation, neither the consumer incentive to return containers nor the obligation to receive them exists.

Across both existing and prospective deposit markets, TOMRA often engages long before legislation is formally implemented. With more than five decades of operating experience, the company today plays an active role in discussions around how new systems are designed and introduced. Tove Andersen explains:

“We see it as part of our role to share our expertise. We have a lot of experience with deposit systems and extended producer responsibility systems, and we drive circularity for other materials too. [...] We have a public affairs team that does advocacy work, working with governments and other key stakeholders, including industry organizations. We share our knowledge and competence on what the key things are to consider to drive the desired result: increased circularity, reduced carbon emissions, and reduced litter.”

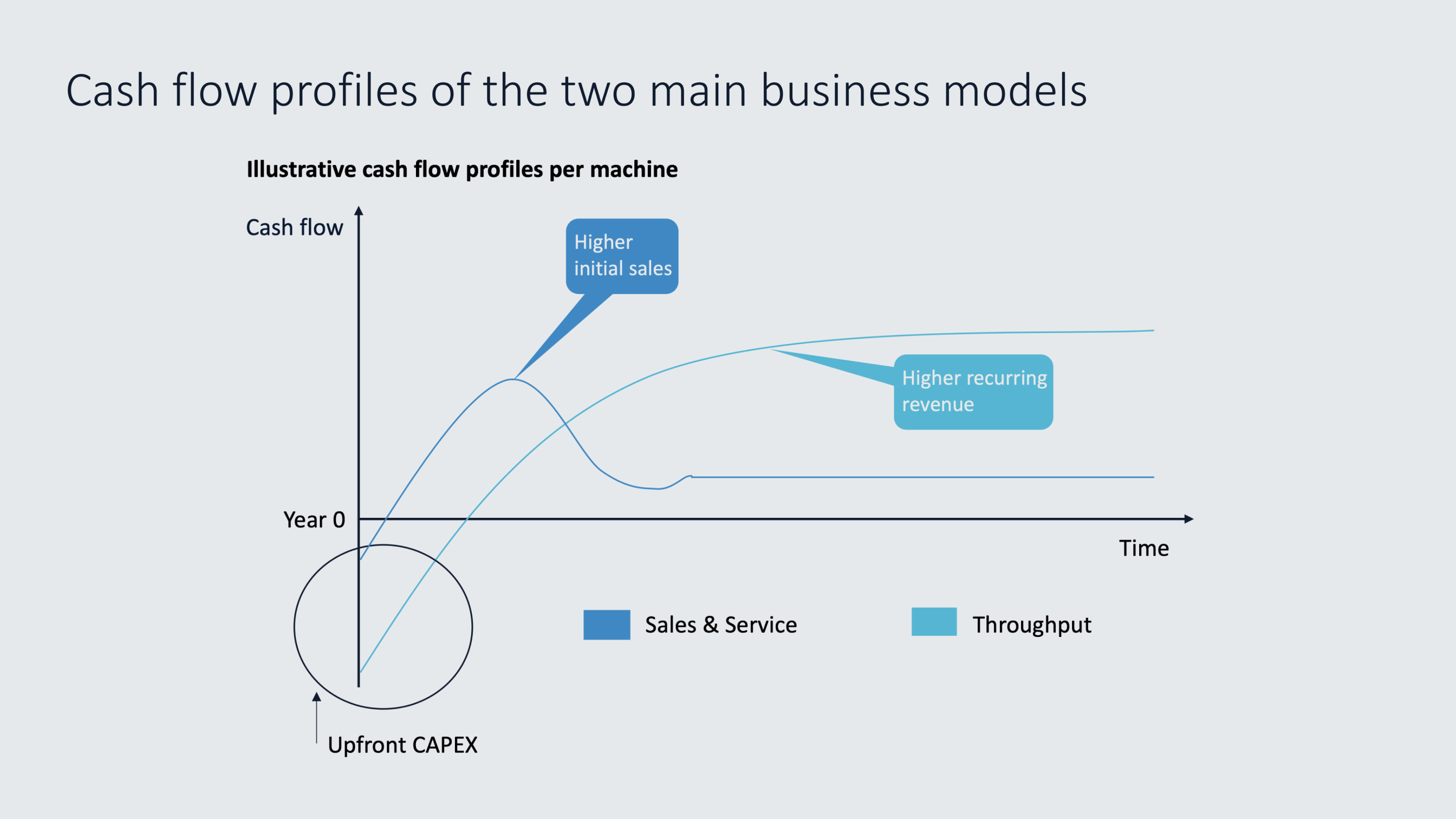

In many of its markets, particularly in Europe, the business model operates in two layers. The first begins with the equipment sale itself. If TOMRA is selected as supplier, the relationship starts with a rollout agreement, often spanning ten years or more. Revenue is recognized when machines are delivered, making this part of the business inherently lumpy: accelerating when new markets launch and slowing as those markets mature. It is the most visible revenue stream, but also the least predictable.

In Norway, Germany, Sweden, and other mature deposit markets, the model has reached further stages. The machines were installed years or decades ago, and the business today is centered more around the installed base and potential upgrades than new lumpy rollout activity. Most recently, TOMRA has entered the early stages of new systems in markets such as Poland and Portugal, shipping machines and building the installed base that over time matures into recurring service revenue.

What follows equipment sales is that second layer of service and maintenance. The sale of a TOMRA RVM is the beginning of a multiyear relationship. Once a machine is installed and running, it needs to be maintained, calibrated, and updated. TOMRA earns a recurring fee for this, tied to the accumulated size of the installed base and largely independent of new sales activity. The margins are strong, the revenue is predictable, and an installed base with machine lifetimes over a decade generates cash flow long after the initial sale.

Over time, switching costs also increase. Mature deposit markets such as Norway, Germany, and Sweden illustrate how TOMRA has deepened its position over the decades. Once a supermarket chain has standardized its operations around one supplier, service integration, employee familiarity, and operational workflows become deeply embedded.

Because TOMRA entered markets at different times and under different structures, its installed base today exists at multiple stages of maturity simultaneously. The result is a revenue mix that gradually shifts over time: less dependent on equipment sales and increasingly weighted toward recurring revenue streams.

Beyond the two-layer model described above, TOMRA operates two additional Collection models: throughput and material recovery. Both represent structurally different commercial arrangements and highlight how the company adapts its model to different market structures.

In several markets, TOMRA does not sell the machine at all. Instead, it retains ownership of the infrastructure, services the machines itself, and earns a handling fee for every container returned through the system, a model TOMRA refers to as throughput. Lithuania, Latvia, Australia, and North American markets operate predominantly under this structure, as does Singapore following the launch of its deposit return system in 2026.

The tradeoff is that throughput requires significantly more upfront capital. In return, however, it creates recurring, volume-linked revenue streams with the potential for stronger long-term economics. On the balance between the different Collection models, Tove Andersen explained:

“We don't want all of our business to be throughput, because we couldn't carry that much capital on our balance sheet. So we think a balance is good. The advantage of throughput is recurring, stable revenue. With sales and service, you have the sale, then a guarantee or warranty period, and then the service revenue. Our view is that a balance is best.”

Collection also includes a revenue stream that exists nowhere else within the group: material recovery. In the northeastern United States and Canada, TOMRA operates further down the value chain, collecting, transporting, and processing returned containers on behalf of beverage producers with legal collection obligations.

The company operates processing facilities across the region, recovering baled aluminum, crushed glass, and PET flakes that are then sold to recyclers. Revenue comes as a fee per container processed plus commodity income tied to the recovered material, making it the most volume- and price-sensitive revenue stream within Collection. It also means the line's profitability can shift meaningfully over time.

Within the Collection division, revenue is split approximately 40% from equipment sales, 20% from service contracts, 20% from throughput, and 20% from material recovery.

If we couldn't have the right solution for a particular market, it's hard to imagine who would. We have the broadest portfolio of any player.— Tove Andersen

Where Collection is built around consumer-facing return infrastructure, Recycling serves industrial customers such as WM or Republic Services, or a plastic recycler, waste processor, or metals sorting facility. The segment sells sensor-based sorting machines installed in large processing facilities, where mixed waste streams are separated by material type and quality so they can re-enter the supply chain as secondary raw materials.

In the aluminum chain, for example, TOMRA's sorting machines distinguish between alloy grades in mixed scrap, preventing downgrading and producing furnace-ready fractions. That material then flows to smelters and rolling mills, which turn it into aluminum can sheet that eventually becomes a new beverage can at a producer like Ball.

TOMRA is a global leader in recycling solutions, serving customers in more than 100 countries with an installed base of approximately 11,900 machines. The division represented just over 15% of group revenue in 2025 and competes mainly with the private companies Pellenc ST and Steinert.

Equipment sales remain the dominant source of revenue in Recycling, but the installed base also generates recurring software and service revenue, which represented roughly 26% of divisional revenue in 2025. Similar to the primary model in Collection, machines require ongoing calibration, maintenance, upgrades, and optimization over their operating lives. Increasing the share of these more recurring revenue streams is a stated strategic priority for TOMRA.

The largest part of the business is waste recovery and plastics recycling: sorting mixed waste streams and pre-processing recovered plastics into homogeneous fractions that can be recycled. The second core application is metals recycling, where sensor-based sorting separates non-ferrous metals such as aluminum, copper, brass, and stainless steel from mixed scrap.

Beyond these two areas, TOMRA also sells into paper, wood, textiles, e-waste, and mining, grouped into reporting buckets alongside the main applications. In the first half of 2024, those buckets split revenue roughly 80/20 in favor of plastics and waste recovery; by the first half of 2025, that had shifted to 60/40 as metals and ore sorting took a larger share.

Compared with Collection, where legislation creates a direct catalyst for equipment sales, Recycling is more exposed to market economics and therefore more sensitive to the macro environment. Customers make investment decisions based on commodity prices, capacity utilization, financing conditions, and regulatory confidence.

There is usually no external deadline forcing a decision in any given quarter, which makes deferral easier. When industrial sentiment weakens, or when aluminum or PET prices remain under pressure, the order pipeline can slow across much of the customer base.

Recycled-content regulation also works differently from a deposit return mandate. A deposit law can require collection infrastructure to be installed in a specific market by a specific date. Recycling regulation is typically more indirect, usually designed with requirements that products or packaging contain a minimum share of recycled material. That creates demand for recycled feedstock, which can improve recycler economics and eventually lead to investment in sorting capacity. But there are more steps in the chain and more places for the logic to stall.

Therefore, cyclicality is one of the defining characteristics of Recycling. Over the coming years, however, regulation is expected to play a growing role in the division. The interplay between that structural tailwind and the near-term cyclical headwinds is something we will return to.

TOMRA Food sells sensor-based sorting and grading systems to harvesters, packers, and food processors. As of 2025, it was TOMRA's second-largest division by revenue at EUR 328 million, accounting for roughly 25% of the group.

The segment focuses on nine food categories where TOMRA sees the greatest value-add potential from its technology: potatoes, nuts, blueberries, kiwifruit, citrus, cherries, apples, processed fruit, and processed vegetables. While citrus has recently seen the strongest growth in order intake, potatoes remain the largest category.

More than two-thirds of all potatoes processed into french fries globally pass through TOMRA's peeling and sorting systems – capabilities built through the acquisitions of Odenberg and BEST – supplying major processors such as McCain Foods and Lamb Weston.

A potato processor, as in the example above, uses a TOMRA sorter to remove foreign objects, defective product, and excess peel. A citrus producer sorts fruit by size, color, and sugar content. A frozen vegetable processor uses the same underlying technology to maintain consistency across millions of units per hour. The systems operate at speeds and levels of precision that are impossible to fully appreciate until seen in real time.

Food has approximately 16,000 installations across around 80 countries and an estimated market share of roughly 30%. Compared with TOMRA's other divisions, Food operates in a more fragmented competitive landscape and is the group's most geographically diversified business, reflecting the global nature of food production and processing. The Americas account for the largest share of revenue, followed by Europe and Asia.

Like all TOMRA machines, its Food systems are incredibly technically sophisticated, combining X-ray, laser, camera, spectroscopy, and AI-based recognition technologies to detect both visible and invisible defects at speeds no human inspection line could match. The latest generation of TOMRA's AI-powered sorters targets a false reject rate below 1%.

A key difference between Food and TOMRA's other divisions is the customer investment case. There is no direct government mandate requiring a food processor to install a TOMRA sorter in the way deposit return legislation drives Collection infrastructure, or recycled-content targets influence Recycling investment. The decision is primarily commercial: improving yield, reducing waste, strengthening food safety, and lowering labor costs.

The commercial structure largely mirrors the primary model of Collection and the Recycling division, beginning with equipment sales and followed by software and service revenue over the lifetime of the installed base. In 2025, equipment accounted for roughly 70% of Food revenue, with software and service making up the remaining 30%.

The aftermarket relationship in Food often runs deep. Sorting lines are calibrated to specific products, quality standards, and production environments, while software and AI models continuously improve sorting precision over time through data and machine learning. Together, this creates significant switching costs once a system is embedded in a customer's operations.

Beyond its three core divisions, TOMRA launched Horizon in 2022 as a business-building portfolio focused on adjacent opportunities within resource optimization and circularity. Tove Andersen described the rationale behind the initiative:

“With Horizon, we looked at large unsolved problems within resource optimization and circularity, where we have a right to win based on our experience, competence, or technology. The key criterion is that the problem must be big enough to, over time, become a new leg for TOMRA. This isn't about small initiatives; it's about making bets that could become large.

Horizon should not be an R&D investment; it's a business-building portfolio. The technology should be more or less ready for scaling. Some technology development is always needed, but it should be at a stage where you can start building a business around it.”

At launch, Horizon focused on Feedstock, Reuse, and Textiles. In 2024, however, TOMRA paused the Textiles initiative after concluding that the market was not yet commercially mature enough to meet Horizon's business-building criteria. The effort was instead transitioned into technology development within the Recycling division, and in its place, smart waste management became a new exploration area.

One example of Horizon's Feedstock ambitions is Områ, a fully automated plastics sorting facility outside Oslo that we visited following our meeting at TOMRA's headquarters in Asker.

Operated as a joint venture between TOMRA and Plastretur, Norway's producer responsibility organization for plastic packaging, Områ is designed to process the country's plastic packaging waste into commercially usable raw material fractions. The plant sorts incoming mixed plastic waste into ten distinct output streams, each pure enough to serve as feedstock for mechanical or chemical recyclers.

Built on the same sensor-based technology platform as TOMRA Recycling, the facility demonstrates how the company's sorting expertise can be applied beyond its traditional equipment business and further into industrial recycling infrastructure.

Across Horizon and its three core divisions, TOMRA continues to see a wide range of opportunities for further development and expansion. As Andersen put it:

“We have so many ideas for things we could improve. I know many industries struggle to find new improvements. We have a long list in all three divisions, so for us it's really about prioritizing. We can't afford to do everything.

In Food and Recycling, ideas can be about new segments to sort or sorting for new things. In Collection, it can be about convenience for consumers or for stores. That's an important part when we talk about capital allocation: how much should we spend on R&D, how much can we afford to spend, and then we have to prioritize within that list.”

Understanding regulation is essential to understanding TOMRA. Throughout the company's history, legislation has shaped which markets exist, how quickly they develop, and how attractive the economics become. That influence has always been strongest in Collection and is becoming increasingly important in Recycling.

For TOMRA, however, regulation affects the two divisions differently. In Collection, legislation creates the market itself by establishing deposit return systems and collection obligations. In Recycling, regulation works more indirectly by influencing demand for recycled material and investment in sorting capacity.

Those differences matter because they shape not only TOMRA's growth opportunities, but also the timing and cyclicality of demand across the business.

Of the EUR 1.3 billion revenue TOMRA generated in 2025, Collection in Europe represented roughly a third of that total. The region remains particularly important because of the regulatory alignment created by the European Union, where legislation can influence dozens of markets simultaneously.

That dynamic has shaped TOMRA's history for decades and will likely shape much of its near future. Other regions also represent opportunities, but tend to move through more fragmented state- or province-level processes with differing timelines and political priorities. Across the world, deposit systems continue to be debated, designed, and implemented at different speeds.

Even within Europe, implementation is far from uniform. EU legislation may establish shared targets, but each country still decides how the system is structured and when it is introduced. The gap between a regulation being adopted in Brussels and infrastructure being installed in supermarkets across an individual country can span years.

The regulatory architecture affecting TOMRA in the European Union rests on two distinct pillars. The first governs how beverage containers are collected, and the second governs what happens to the material once it has been collected.

As touched on earlier, the EU had already introduced the Packaging and Packaging Waste Directive in the early 2000s to encourage higher recycling rates. But because the framework carried no binding mandates and left implementation largely to individual governments, broader adoption of deposit systems did not follow.

The more consequential shift came with the EU's Single-Use Plastics Directive, adopted in 2019. Among its provisions was a binding collection target for plastic beverage bottles: member states must collect 90% of bottles placed on the market by weight by 2029.

In 2024, that target was extended to include metal cans through the Packaging and Packaging Waste Regulation. The targets apply regardless of whether a country already operates a deposit system, with member states facing EU infringement proceedings if they fall short.

TOMRA's experience operating deposit systems across different markets has led the company to conclude that legislation is foundational to achieving those collection levels. As Tove Andersen explained to us:

“For deposit systems, we believe legislation is necessary. Our experience is that voluntary schemes don't work because you don't reach the necessary scale, and the system becomes very inefficient.”

Andersen made a similar point at TOMRA's 2024 Capital Markets Day, stating that “deposit return systems are the only proven solution to achieve more than 90% collection rates of beverage containers.” What she refers to is decades of evidence showing that countries relying on curbside collection, public recycling points, or voluntary return systems consistently come in far below that level.

These statements are well-supported by evidence from markets ranging from Norway and Germany to the Baltic states and Australia. Without the financial incentive, markets don't come near those numbers. The EU's 2029 target has therefore effectively written deposit return systems into the future of every member state.

Several countries have already acted. Hungary, Romania, Ireland, Austria, Poland, and Portugal introduced systems in recent years and are currently at different stages of rollout. Outside the EU, the UK passed its deposit regulation with a planned October 2027 launch.

The remaining holdouts are among the markets that matter most: France decided against a deposit system in 2023, Spain has a legal trigger after missing its 2023 collection target but has yet to confirm a launch date, and Italy still lacks legislation entirely. Together, they represent three of the EU's four largest economies and some of its largest beverage markets.

The EU's Packaging and Packaging Waste Regulation also matters for TOMRA's Recycling division, where plastics account for a large share of activity. By 2030, plastic packaging sold in the EU must contain at least 30% recycled content, compared with a current European average of around 10%.

Meeting those requirements at an industrial scale depends on advanced sorting technology. Recyclers need to process collected material into fractions pure enough for food-grade and other contact-sensitive applications, which is where TOMRA's systems become relevant.

The mechanism, however, differs from Collection. A deposit law can create a direct equipment need: a retailer must install reverse vending infrastructure by a specific deadline. A recycled-content mandate works further downstream by increasing demand for recycled plastic, improving the economics of high-quality recyclate, and eventually supporting investment in sorting capacity.

That extra distance matters. As touched on, investment decisions in Recycling have so far remained more exposed to commodity prices, customer CapEx cycles, financing conditions, and industrial confidence. The regulatory direction is clear, but the timing of equipment orders is less direct than in Collection.

While Food is driven primarily by commercial logic, Collection and Recycling are both shaped, to different degrees, by regulation. Across both divisions, the gap between where Europe's packaging and waste systems stand today and where 2030 targets require them to be represents a significant opportunity for TOMRA.

For much of the early 2020s, all three divisions carried strong momentum, supported by regulation, automation trends, and broader industrial modernization. More recently, however, parts of the business have faced a more challenging environment. Food softened around 2023 as customers delayed investment decisions, but the most prolonged slowdown has been in Recycling.

All downturns create opportunities, and it's about capturing them and making sure we do better than our competitors, regardless of whether the cycle is up or down.— Tove Andersen

Through the early 2020s, several forces aligned in Recycling. The EU tightened recycled-content requirements while global brands made increasingly ambitious circularity commitments, turning plastic waste into one of the defining environmental themes of the decade. At the same time, the industrial sorting infrastructure needed to deliver on those ambitions barely existed at scale.

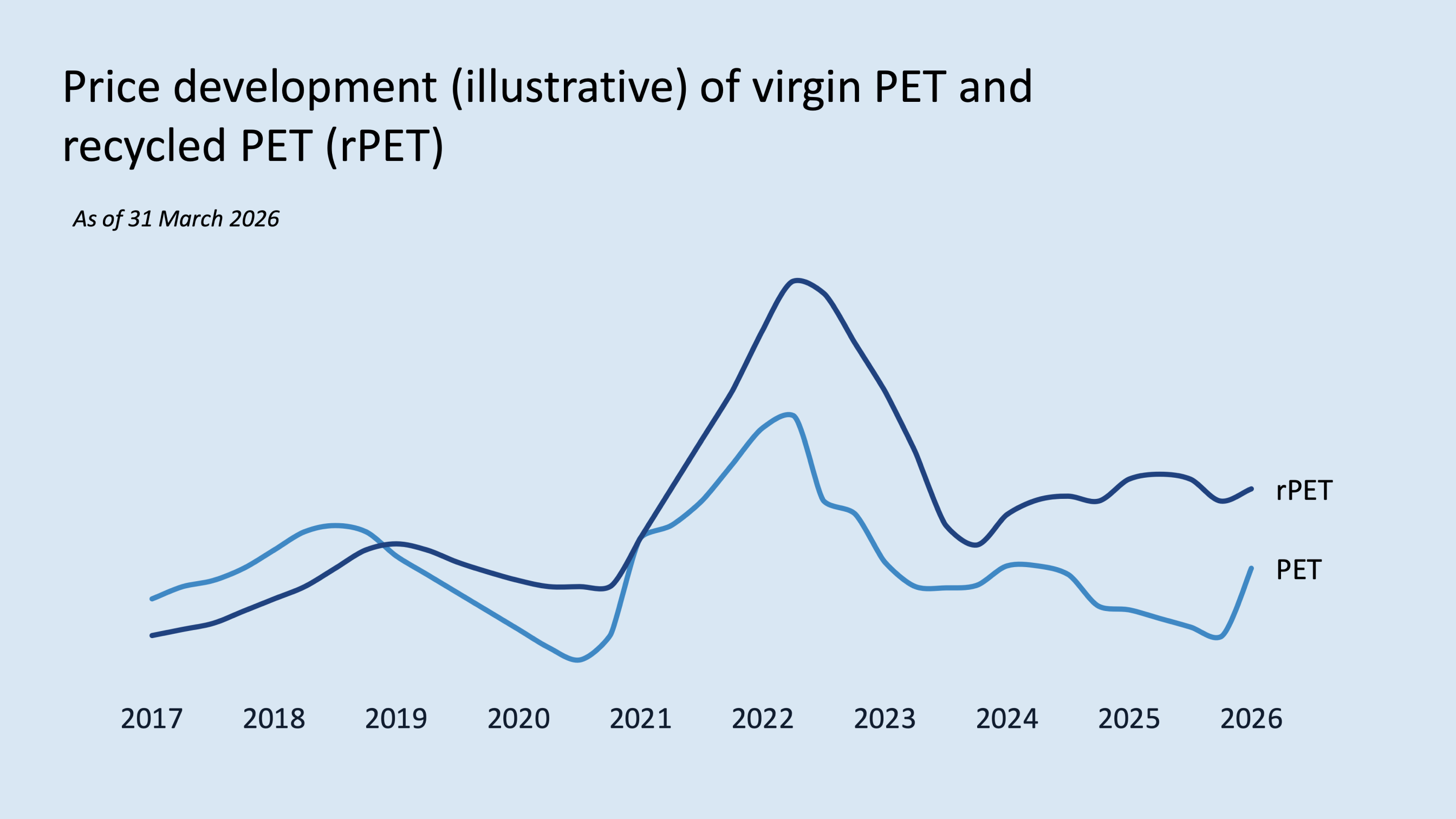

Market economics reinforced the trend. Through 2021 and into 2022, both virgin PET and recycled PET prices rose sharply, and rPET commanded a premium over its virgin equivalent. Both conditions mattered: the premium signaled strong demand for recycled content, while high absolute prices meant operators could justify the capital cost of new sorting and recycling capacity. When both aligned, the investment case was straightforward.

TOMRA entered that period as the dominant technology provider positioned to benefit from the investment cycle, and the Recycling division grew at a 19% CAGR from 2020 to 2023.

Then the cycle turned.

PET prices topped in 2022 and fell sharply through the years that followed. Weaker industrial demand, softer economic conditions in Europe, and broader macro uncertainty compressed the premium that had supported years of investment in recycling infrastructure. Without a clear economic advantage for recycled material, payback periods on new sorting equipment lengthened, and customers increasingly delayed investment decisions.

That dynamic is explained by the indirect structure of Recycling regulation. In the EU, the Packaging and Packaging Waste Regulation creates demand for recycled material, but the effect reaches TOMRA only after moving through recycler financing decisions. Compared with Collection, there are simply more steps in the chain and therefore more opportunities for delay.

TOMRA felt this directly. Order intake in Recycling weakened through 2024 and declined sharply in 2025. Revenue fell 18% and margins deteriorated. The division's exposure to plastics had amplified growth during the upcycle, but now worked in the opposite direction. Global tariffs added further pressure by weakening customer confidence and giving procurement teams another reason to postpone already deferrable CapEx decisions. Tove Andersen explained:

“Projects aren't being canceled, just pushed out in time. You see this across all industries, selling into CapEx investments right now. Companies are looking at their CapEx plans and delaying what they can, given current macroeconomic uncertainty around inflation and interest rates.”

How long the weakness persists is impossible to predict, and as long as uncertainty remains elevated, customers are likely to continue delaying investment decisions. While Recycling is a global business, Europe consistently accounts for more than half of divisional revenue, which adds another dimension to the downturn. The same region where sentiment has been weakest is also where regulation is becoming more demanding.

The 2030 targets remain fixed regardless of commodity prices or industrial sentiment. As the deadline approaches, the room for deferral narrows. The direction of travel appears clear, even if the timing of customer investment decisions remains uncertain. As Andersen put it:

“We still believe the fundamental drivers are strong. European legislation requires at least a doubling of capacity before 2030. I also think that with the whole focus on supply security and import independence, circularity continues to have strong drivers. We don't expect the market to pick up this year, and possibly not next year either.

We know things don't move linearly. After significant investment cycles, there's a slowdown, then it comes back. For us, it's about focusing on the segments that are working now and making sure we're positioned for when others come back.”

)

While Recycling has faced a more challenging environment in recent years, Collection has remained comparatively stable. Like Recycling, Collection is heavily weighted toward Europe, which has accounted for roughly 58% of divisional revenue in recent years. But unlike the more market-driven Recycling segment, Collection has a stronger structural base, largely independent of industrial capital cycles. Part of that comes from service contracts and machine replacements in mature systems, and the other part comes from opportunities to gain market share as new government-mandated deposit markets are introduced.

Although several regions offer long-term opportunities for TOMRA, the EU currently shapes much of the Collection narrative. The Single-Use Plastics Directive and the Packaging and Packaging Waste Regulation have created a cycle of their own: one driven by legislation rather than commodity prices or customer CapEx sentiment. Revenue can spike when new markets launch, then normalize as those markets mature.

In that environment, TOMRA is well-positioned. The question is not whether the opportunity exists, but how much of it TOMRA can capture as competition increases. The company is the pioneer and market leader, but when several markets are moving toward mandated deposit systems at the same time, competitors naturally follow.

Poland's rollout is one example, with TOMRA entering alongside several other players and competing for share. Andersen acknowledged this dynamic at the company's Q1 2026 earnings call (sourced through Quartr Pro):

“We knew that there would be tough competition in the new markets. We knew that there would be price pressure. It is important for us to get a large share initially at the same time as we want to maintain our margins. So this is a balance that we are playing when we are then deciding our commercial tactics in the different markets.”

It is a deliberate balancing act, and one that will play out differently across each EU market. TOMRA understands that defending its leading position requires constant innovation, Andersen explains:

“Unless you innovate, you'll always face margin pressure; that's just how business works. When you launch something in a market, competitors will develop something similar within a certain period, and you'll face price competition and inflation. So you need to constantly work on your COGS to mitigate inflation. To maintain margins over time, you need to innovate.”

TOMRA will not sacrifice margins indiscriminately to win share, but it is also aware of what is at stake in the early stages of a new market. Customers signed at launch tend to stay with service contracts that run for years, integrations that deepen, and, as we've been over before, the cost of switching increases over time. That is the strategic logic behind accepting some short-term margin pressure in new markets. Scale also strengthens the service network, creating a feedback loop between market share, operational efficiency, and customer loyalty. As Andersen put it:

“Scale is important for the service organization. That's why we have an ambition that we should always be the significantly largest player in a country, because that gives us a much better scale than competitors. That is so important for customer satisfaction and for building loyalty.

There's the initial rollout, where you install a certain number of machines that typically last 7 to 10 years before replacement cycles begin. But retailers are also constantly closing and opening stores, so there are always sales opportunities. Strong operational delivery is what creates that loyalty.”

While recent years have shown how narratives can drive the discourse (and valuations) around sustainability-driven companies such as TOMRA, the broader need for resource optimization continues to move in one direction. Over more than five decades, TOMRA has navigated shifting political agendas, regulatory cycles, and changing market conditions while continuously adapting its business to where that direction is heading. As Tove Andersen put it:

“TOMRA has always had a can-do attitude. If a challenge is thrown at the organization, [we'll] solve it.”

Since entering the pandemic with its three new core divisions in place, the company has experienced both strong momentum and a series of operational challenges. On 16 July 2023, TOMRA was hit by a major cyberattack that affected its domain and several key IT systems, forcing the company to proactively disconnect services until systems could be validated and restored. The response limited the lasting impact, but the incident showed the operational complexity that comes with supporting more than 120,000 machines globally.

Food, meanwhile, entered a softer period through 2023 as customers delayed investment decisions amid a weaker macroeconomic environment, high interest rates, and poor harvests. The slowdown accelerated a restructuring effort that had been building since the acquisition-heavy years of the 2010s, leading to a consolidation of the division's operating structure. Then came the Recycling downturn described earlier. In response, TOMRA launched an additional cost-reduction program at the start of 2026.

Collection has always been the core of TOMRA, and that is likely to remain true in the years ahead. Across the EU, deposit systems continue to launch market by market, each adding thousands of machines to an installed base that can generate service revenue for years. The direction of travel is clear. The regulatory environment that has shaped TOMRA's growth for more than five decades continues to expand.

)

More than fifty years ago, the Planke brothers built a machine to solve an operational problem for a Norwegian grocer overwhelmed by empty bottles. Over the decades, that innovation grew into global infrastructure for sorting, recovering, and recirculating resources. The machines are more advanced, the markets are larger, and the materials now stretch far beyond bottles and cans. But the core idea that started in Asker still runs through TOMRA.

Explore our platforms

Leading companies and financial institutions worldwide rely on Quartr to make better decisions faster.

Desktop

API

)

)

)